CEO Morning Brief

Baltic Exchange Shipping Updates: Aug 2, 2024

edgeinvest

Publish date: Tue, 06 Aug 2024, 09:30 AM

A weekly round-up of tanker and dry bulk market (August 2, 2024)

This report is produced by the Baltic Exchange.

The Baltic Exchange, a wholly-owned subsidiary of Singapore Exchange, is the world's only independent source of maritime market information for the trading and settlement of physical and derivative contracts.

Its international community of over 650 members encompasses the majority of world shipping interests and commits to a code of business conduct overseen by the Baltic.

For daily freight market reports and assessments, please visit www.balticexchange.com.

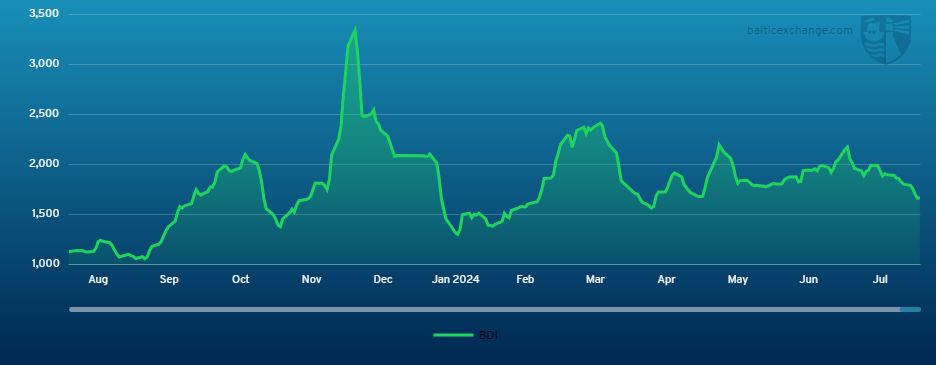

Capesize

The week commenced with a tepid start as the BCI 5TC index slipped, reflecting limited activity in both regions. As the days progressed, the Pacific saw a reasonably robust list of available cargoes, although activity was still somewhat stagnant. Midweek, the market faced challenges despite heightened activity, with the BCI 5TC index experiencing a notable drop, sliding US$1,017 to settle at US$19,717. Ample tonnage availability in the Pacific hindered any potential gains, while weaker fixtures in the Atlantic further pressured the market. Towards the end of the week, the Pacific showed signs of stability with all miners active and an increase in coal cargoes. Despite decent volumes, the market struggled to gain momentum. However, by Friday a couple of stronger fixtures were reported resulting in the C5 index finishing the week at US$9.820. Overall, the week concluded on a mixed note. Conditions in the Atlantic remained subdued, while the Pacific showed slight improvement, leading to a US$313 increase in the BCI, which settled at US$19,299.

Panamax

A compelling week in the Panamax market. The North trans-Atlantic runs providing numerous points of discussion, with wide ranging views on where true market value lay. Tight tonnage count this side persisted all week, whilst those owners looking to minimise duration and secure positioning for latter contracts, securing the few mineral voyage cargoes available. Unsurprisingly returning a heavily discounted equivalent way below index levels. An underwhelming week ex-South America, with only a brace of end August arrival deals concluded basis delivery APS load port basis around the US$19,000 + US$900,000 mark. The Asian basin saw decent volume ex-Australia and Indonesia, however tonnage particular in the North of the region forcibly keeping a lid on rates. A mix of rates emerging ex-Australia, the median rate overall came to around the US$14,000 mark. Period activity overall but did include reports of an 82,000-dwt delivery China agreeing US$18,250 basis 5/7 months trading.

Ultramax/Supramax

A rather uneventful week for the sector as the ‘summertime blues’ kicked in. The recent upturn from the US Gulf ended as demand fell away putting downward pressure on rates. The South Atlantic also lacked much fresh impetus with rates hovering around last down. The Continent - Mediterranean was seen as positional with limited fresh enquiry appearing. From Asia, a fairly similar story but some said it was a bit more positional. As the week progressed, the Indonesian coal demand slipped down and prompt tonnage lists grow. A 55,000-dwt fixing delivery Koh Sichang for a trip via Indonesia redelivery WC India at US$13,000. Further north, there was intermittent demand, with a 63,000-dwt open China fixing a trip via Gulf of Aden redelivery Mediterranean at US$16,000 for the first 65 days and US$18,000 for the balance. For NoPac business a 58,000-dwt open Japan fixed a soda ash run via NoPac redelivery Southeast Asia at US$14,000. The Indian Ocean remained fairly subdued, with a 60,000-dwt fixing delivery Hamriyah trip via Arabian Gulf redelivery WC India in the mid US$18,000s. It was also noted that with the general lack of demand, period activity also dropped off as many players waited to see is the fundamentals may change.

Handysize

With the Summer holiday season in the Northern hemisphere and the Olympic games in Paris, it has been only what can be described as a rather uneventful week for the sector. The Atlantic was rather positional. Some felt that a slight upward trend remained both from the US Gulf and South Atlantic, although it was patchy. A 38,000-dwt rumoured fixed in the mid US$19,000s for an Upriver Plate trans-Atlantic run. However, it also surfaced that a 35,000-dwt fixed from North Brazil to the Mediterranean at around US$15,000. The Continent-Mediterranean lacked fresh impetus but a 40,000-dwt fixed delivery United Kingdom trip via the Baltic redelivery West Africa (non HRA) in the mid US$15,000s. From Asia, as the week progressed, brokers said it was becoming increasingly evident that lower cargo volumes were being felt and that the amount of prompt tonnage increased. From the Indian Ocean, limited action again saw a 32,000-dwt fixed delivery Damman for a trip via the Arabian Gulf redelivery EC India at US$11,000.

Clean

LR2

LR’s in the MEG continued to trundle along stable this week. The 75Kt MEG/Japan TC1 index floated around the WS150 mark. The 90kt MEG/UK-Continent of TC20 is also coasted along at the US$4.4m - US$4.6m position all week.

West of Suez, Mediterranean/ LR2’s on TC15 maintained their recumbency at US$4.2m for the second week on week.

LR1

In the MEG, LR1’s remained relatively flat this week. The 55kt MEG/Japan index of TC5 continued to hover around the WS155 level while the 65kt MEG/UK-Continent of TC8 did dip US$100,000 to US$3.73 million. On the UK-Continent, the 60Kt ARA/West Africa TC16 index lingered prostrate in the high WS140’s.

MR

MR’s in the MEG ticked along with just enough enquiry to prevent softening. The 35kt MEG/East Africa TC17 index, as a result, resided at WS200 all week.

UK-Continent MR’s looked as though they were going to recover mid-week. The 37kt ARA/US-Atlantic coast of TC2 peaked at WS211 mid-week but then returned quickly back to the WS200 level. TC19 (37kt ARA/West Africa) similarly hopped up to WS230 at the same time and then dropped back to WS220 by the end of the week.

The USG MR’s were by comparison to recent behaviour relatively flat this week. Within the week TC14 (38kt US-Gulf/UK-Continent) stayed around the WS155-165 level. The 38kt US-Gulf/Brazil of TC18 did by comparison drop 15 points from WS242 to WS227 and the 38kt US-Gulf/Caribbean TC21 was assessed around the US$677,000-750,000 range all week.

Handymax

In the Mediterranean, Handymax’s took a heavy hit and TC6 30kt Cross-Med lost 59 points to WS156. Up in northwest Europe, the TC23 30kt Cross UK-Continent shed 15 points to WS191.

VLCC

The VLCC market fell away this week, losing recent gains. The 270,000 mt Middle East Gulf to China trip lost eight points to WS47, corresponding to a daily round-trip TCE of US$23,656 basis the Baltic Exchange’s vessel description.

In the Atlantic market, the rate for 260,000 mt West Africa/China eased five points to WS52.39 (which shows a round voyage TCE of US$30,028/day), whilst the rate for 270,000 mt US Gulf/China was reduced by US$335,000 to US$7,100,000 (US$30,929/day round trip TCE).

Suezmax

Suezmaxes in West Africa were again weaker this week, with the rate for 130,000 mt Nigeria/UK Continent dropping another seven points to WS80.39 (a round-trip TCE of US$26,268/day). Baltic Exchange has introduced a new route (TD27) from Guyana to UK Continent basis 130,000mt, which was assessed on Thursday at WS80.56, giving a daily round trip TCE of US$26,034 basis discharge in Rotterdam. In the Mediterranean and Black Sea region the 135,000 mt CPC/Med route slipped a further 2.5 points to about WS97.5 (showing a daily TCE of just below US$31,000 round-trip). In the Middle East, the rate for 140,000 mt Middle East Gulf to the Mediterranean (via the Suez Canal) remained around WS85.

Aframax

In the North Sea, the rate for the 80,000mt Cross-UK Continent held at the WS120 level (translating to a daily round-trip TCE of a little over US$23,200 basis Hound Point to Wilhelmshaven).

In the Mediterranean market the rate for 80,000mt Cross-Mediterranean recovered recent losses, gaining 18.5 points to WS146.67 (basis Ceyhan to Lavera, that shows a daily round trip TCE of about US$37,800).

Across the Atlantic, the market continues to collapse. For the 70,000mt East Coast Mexico/US Gulf (TD26) the rate fell a further 71.5 points to WS128.33 (a daily TCE of US$17,851 round trip) while the rate for 70,000mt Covenas/US Gulf (TD9) capitulated 62.5 points to WS118.44 (a round-trip TCE of US$18,145/day). The rate for the trans-Atlantic route of 70,000mt US Gulf/UK Continent (TD25) lost almost 25 points to WS128.33 (a round trip TCE basis Houston/Rotterdam of US$24,742/day).

LNG

The Pacific market has pulled away a little regaining some of the lost ground against the Atlantic recently. With low supply of 2-stroke 174cbm tonnage in the Asia region the BLNG1-174 index rose by US$2,300, the largest movement of any route this week and closed at US$76,100, while the BLNG1-160 languished moving nothing at all, closing again at US$61,000.

News of the Freeport LNG terminal getting all three of its trains back up and running, hinting at a possibility of recovering normal production rates, hasn’t done anything to move the rates. Both the BLNG2-160 and BLNG174 lost US$600 to a close of US$57,700 and US$73,800, respectively. With vessels in supply and only reports of a TFDE 160cbm ship on subs for a late August US-Europe stem there hasn’t been much driving a gain. For Houston-Japan BLNG3 the 174cbm was flat moving zero at US$88,400 while the 160cbm fell a few hundred dollars to US$73,000.

Period hasn’t been seeing much play as is usual for the summer months, and we published six-months US$100,800, one-year US$81,500 and the three-year at US$84,000, all of which are down from the previous week.

LPG

A rather slow week in the MEG with BLPG1 falling US$5.166 to US$46.667 making the publication the lowest we have seen since back in early February. A slow fixing week, coupled with more vessels than expected, has put pressure on rates and as a result we have seen a firm downward trend. One vessel reported on subs around US$45 hasn’t lowered the index there yet but it will not be unexpected if we are to move further down.

For the Atlantic routes there has been a few more fixtures done basis BLPG2 Houston-Flushing than we have seen for many weeks. With around four ships with options going to Flushing there has been more interest but rates haven’t really reacted. For Houston-Chiba BLPG3 there was only a movement of a few cents with a final close at US$90.417 and a daily TCE earning equivalent of US$27,782. Reports that the Panama Canal Authority will reopen the canal crossings fully within the coming months has alleviated some of the tonne miles but with product long there needs more to move rates higher. BLPG2 Houston-Flushing ended positive, if only by US$0.375 cents and a close of US$49.75 with a daily TCE earning of US$43,827.

Disclaimer:

While reasonable care has been taken by the Baltic Exchange Information Services Limited (BEISL) and The Baltic Exchange (Asia) Pte. Ltd. (BEA, and together with BEISL being Baltic) in providing this information, all such information is for general use, provided without warranty or representation, is not designed to be used for or relied upon for any specific purpose, and does not infringe upon the legitimate rights and interests of any third party including intellectual property. The Baltic will not accept any liability for any loss incurred in any way whatsoever by any person who seeks to rely on the information contained herein.

All intellectual property and related rights in this information are owned by the Baltic. Any form of copying, distribution, extraction or re-utilisation of this information by any means, whether electronic or otherwise, is expressly prohibited. Persons wishing to do so must first obtain a licence to do so from the Baltic.

Source: TheEdge - 6 Aug 2024

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on CEO Morning Brief

Singapore Banks Back Police Controls on Accounts to Avert Scams

Created by edgeinvest | Jan 10, 2025

Trader Who Made Billions in 2008 Returns to Bet on Market Swings

Created by edgeinvest | Jan 07, 2025

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

RHB Investment Research Reports

2

3

SGX Market Updates

STI Begins New Year With 1.8% Return, Led by Singtel & Seatrium

4

SGX Market Dialogues

5

SGX Market Dialogues

10 in 10 With GSS Energy - Exploring New Segments for a Turnaround

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....