Trader Hub

DBS Group Holdings Ltd – Continued NIM Growth Boosts NII

traderhub8

Publish date: Fri, 04 Aug 2023, 10:59 AM

- 2Q23 adjusted PATMI of S$2.69bn was above our estimates due to higher net interest income (NII). 1H23 adjusted PATMI is 57% of our FY23e forecast. 2Q23 DPS is raised 33% YoY to 48 cents, bringing 1H23 dividend to 90 cents. We raise our FY23e DPS from S$1.68 to S$1.86.

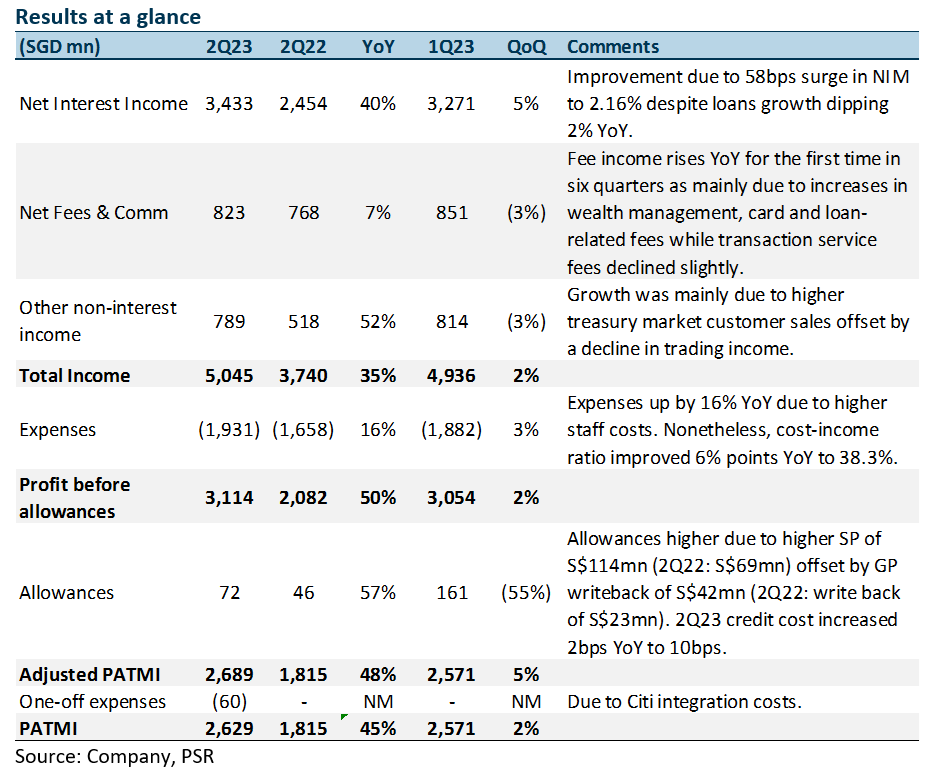

- NII surged 40% YoY to S$3.43bn on NIM expansion of 58bps to 2.16% despite loan growth dipping 2% YoY. Fee income rose 7% YoY, the first YoY increase in six quarters, while other non-interest income grew 52% YoY. DBS increased its NIM guidance from 2.05-2.10% to around 2.15%, lowered loan growth guidance from 3-5% to low single-digit and maintained fee income guidance at high-single digit for FY23e.

- Maintain BUY with an unchanged target price of S$41.60. We raise FY23e earnings by 9% as we raise NII estimates for FY23e due to higher NIMs, offset by lower fee income, higher provisions, and higher expenses estimates. We assume 1.90x FY23e P/BV and ROE estimate of 16.6% in our GGM valuation.

The Positives

+ NIM and NII continue to increase. NII spiked 40% YoY to S$3.43bn due to a NIM surge of 58bps YoY to 2.16% (3Q22: +32bps, 4Q22: +15bps, 1Q23: +7bps, 2Q23: +4bps) despite loan growth dipping 2% YoY. Increases in non-trade corporate loans were offset by lower trade loans. Housing loans were stable, while wealth management loans declined modestly. Management spoke of an upside bias to NIM from its current levels and indicated that NIM will likely peak in 2H23.

+ Fee income rose 7% YoY, first in 6 quarters. Fee income increased 7% YoY, the first YoY increase in six quarters. WM fees increased 12% YoY to S$377mn from higher bancassurance and investment product sales. Card fees grew 17% YoY to S$237mn from higher spending including for travel while loan-related fees rose 17% YoY to S$133mn. These increases were moderated by a 5% YoY decline in transaction service fees led by trade finance.

+ Other non-interest income rose 52% YoY. Other non-interest income rose 52% YoY mainly due to an increase in net trading income from higher trading gains and an increase in treasury customer sales to both wealth management and corporate customers. Additionally, gains from investment securities more than doubled due to improved market opportunities.

The Negatives

– Allowances rose 57% YoY. 2Q23 total allowances were higher 57% YoY due to an increase in SP to S$114mn (2Q22: S$69mn) offset by higher GP write-back of S$42mn for the quarter (2Q22: write-back of S$23mn). Resultantly, 2Q23 credit costs rose by 2bps YoY to 10bps. Nonetheless, the NPL ratio declined to 1.1% (2Q22: 1.3%) as new NPA formation fell by 39% YoY. GP reserves rose slightly to S$3.80bn, with NPA reserves at 127% and unsecured NPA reserves at 224%.

– CASA ratio decline continues. The Current Account Savings Accounts (CASA) ratio fell 14.9% points YoY to 51.5%, mainly due to the high interest rate environment and a continued move towards fixed deposits (FDs). Resultantly, total customer deposits fell 2% YoY to S$520bn as the decline in CASA deposits were partially offset by growth in FDs.

Source: Phillip Capital Research - 4 Aug 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Apps

Top Articles

1

SGX Market Dialogues

10 in 10 With NetLink NBN Trust - The Fibre of a Smart Nation

2

CEO Morning Brief

3

CEO Morning Brief

Singapore Airlines’ CEO Gets Pay Jump After Record Annual Profit

4

CEO Morning Brief

5

SGX Market Updates

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....