Trader Hub

Keppel Corporation Ltd – Stable Energy Sales, Weak Real Estate Markets

traderhub8

Publish date: Mon, 23 Oct 2023, 11:40 AM

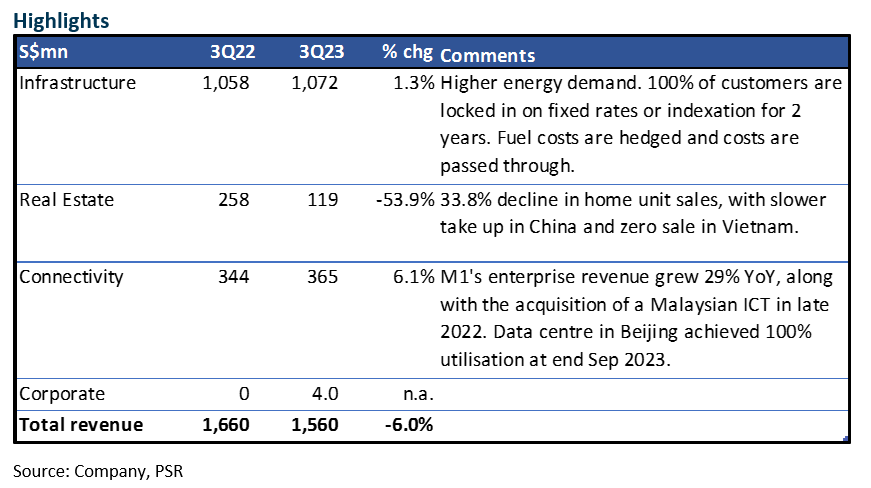

- 3Q23 revenue fell 6.0% YoY, dragged lower by weak property sales in China and India, after the rebound in 1H. 3Q23 net profit was higher YoY, but no financial detail was provided.

- The distribution-in-specie of 1 KREIT unit for every 5 Keppel shares has been approved by shareholders. This is equivalent to S$0.18 per Keppel share.

- Upgrade to BUY due to recent price correction. We maintain our earnings projections. After accounting for the KREIT distribution, our TP is revised lower to S$7.52 (prev. S$7.70).

The Positives

+ 3Q23 Infrastructure revenue grew 1.3% YoY, in spite of a volatile gas price and the implementation of temporary price control measures. 100% of its customers for integrated power sales are locked in on fixed rates, or indexed electricity price plans, for next 2 years. This provides stability to 68% of the group’s revenue. The fuel input costs are hedged, and costs are passed through, including the higher carbon taxes in 2024.

+ M1 expanded customer base by 7.2% YoY to 2,548. It grew enterprise revenue by 29.4% YoY, due to the acquisition of a Malaysian ICT in late 2022.

The Negatives

– Real estate 3Q revenue fell 53.9% YoY, as reflected in the weak property sentiment and rising interest rates. 3Q23 home unit sales fell to 260 units in China (1H23: 1,200 units) and 160 units in India (1H23: 870 units). No sales were recorded in Vietnam for this year.

– Net gearing rose to 0.89x from 0.86x at Jun 2023, after the distribution of interim dividend.

Source: Phillip Capital Research - 23 Oct 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Apps

Top Articles

1

2

RHB Investment Research Reports

3

CEO Morning Brief

China's CICC Eyes Southeast Asia Expansion in Bid to Ease Domestic Woes

4

RHB Investment Research Reports

Food Empire - Slight Negative on Proposed Notes Issuance; BUY

5

SGX Market Updates

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....