Trader Hub

Singapore Telecommunications Ltd – Bruised by Currency

traderhub8

Publish date: Mon, 26 Feb 2024, 11:13 AM

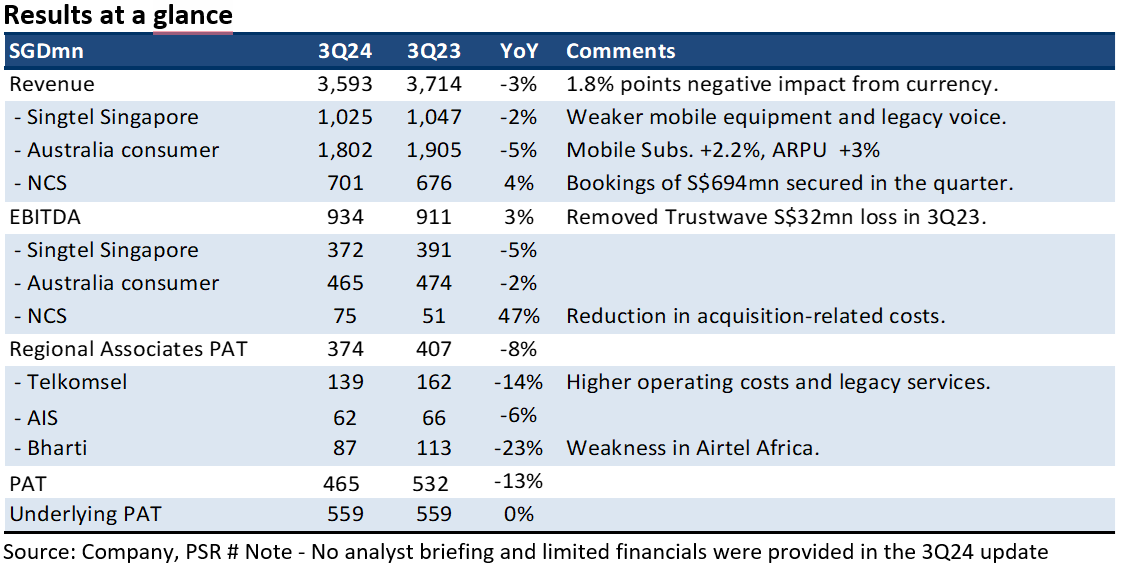

- 3Q24 earnings were within expectation. 9M24 revenue and EBITDA were 73%/75% of our FY24e forecast. Currency was almost a 2% point drag to earnings.

- 3Q24 associate contribution disappointed with an 8% YoY decline to S$374mn. Airtel Africa suffered a YTD24 translation of S$130mn following a massive depreciation of the Nigerian Naira during the quarter. Direct stake in Airtel Africa has been divested.

- We maintain BUY with an unchanged target price of S$2.80. We lowered our associate earnings by 10% due to the weakness in Airtel Africa. But this was offset by a lower finance expense assumption. Our FY24e PATMI is reduced by 3%. We expect an upside surprise in EBITDA margins in 4Q24 if Singtel can deliver its S$200mn of cost out by the end of FY24. Mobile price repair is underway in multiple countries where Singtel operates. We expect this to drive earnings together with plans to monetise S$4bn of assets further.

The Positive

+ Early mobile price repair in Australia. Optus postpaid ARPU of A$42 is the highest in more than four years. We believe price repair is underway. Competition, especially for entry-level price plans, has eased, and prices are edging higher. Despite the network outage, mobile service revenue grew 3.4% YoY.

The Negative

– Airtel Africa currency hit. Contribution from Bharti Telecom declined 23% YoY to S$87mn. Operations in India grew 14% YoY supported by an 8% rise in ARPU to Rp208. Currency took a toll on the results, with a 4% decline in the rupee against the Singapore dollar. A translation loss hit Africa operations due to the weakness in the Nigerian Naira.

Outlook

We expect mobile price recovery in Australia, India, Thailand, and Indonesia to drive earnings growth. An upside surprise in margins will stem from Singtel’s planned S$600mn reduction in core cost, largely in Optus.

Maintain BUY with unchanged TP of S$2.80

Our SOTP valuation is based on 6x EV/EBITDA (in line with peer valuation) for Singtel’s core Singapore and Australia businesses, and associates are marked to market after a 20% discount to reflect volatility in their share prices.

Source: Phillip Capital Research - 26 Feb 2024

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

RHB Investment Research Reports

OCBC Bank - All Eyes On Dividend And Capital Management Plans

2

THE SINGAPOREAN INVESTOR

Mapletree Pan Asia Commercial Trust's 3Q & 9M FY2024/25 Results Review

3

RHB Investment Research Reports

4

THE SINGAPOREAN INVESTOR

A Review of Frasers Centrepoint Trust's 1Q FY2024/25 Business Update

5

SGX Market Updates

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....